Overview and Key Takeaways

The new National Instrument 51-107 Disclosure of Climate-related Matters (NI 51-107), if released year as announced by the legislators, will be a significant development for Canadian capital markets: for the first time, reporting issuers in Canada will be subject to mandatory disclosure of climate-related issues. Climate-related disclosure is also expected to be made mandatory in Initial Public Offerings (IPOs) prospectuses.

In Part 1 of this series, we explored what NI 51-107 may mean for IPO prospectuses going forward. In this Part 2, we explore how ESG issues have been addressed in offering prospectuses to date. We do so because (1) ESG-related disclosure in prospectuses has become more common in recent years even in the absence of specific ESG disclosure requirements, and (2) even if NI 51-107 is issued, general securities law principles requiring the disclosure of material matters in prospectuses, including those involving ESG issues, will continue to apply.

Our key practical takeaways for public issuers in Canada include:

- The most common ESG-related issues addressed in prospectuses were, in order of frequency: (1) sustainability generally, (2) climate change, and (3) Indigenous matters.

- ESG disclosure in prospectuses appears to be industry-agnostic, with substantial ESG-related disclosure occurring in 15 of 20 different industry categories. Somewhat surprisingly, the industry with the highest frequency of substantial ESG-related disclosure was Technology & Software, with the Mining industry following closely.

- Offerings on the TSX were significantly more likely to include substantial ESG-related disclosure than TSX-V offerings. Similarly, the larger the amount of funds raised, the more sophisticated and more detailed the issuer’s ESG disclosure generally was. This indicates that the degree of ESG-related disclosure is in part driven by a cost-benefit analysis.

Our more detailed analysis and commentary follows. For additional related information, see Fasken’s guide to IPOs and Going Public in Canada. For Fasken’s other capital markets thought leadership, visit our Capital Markets and M&A Knowledge Centre.

Methodology

Our sample consisted of 101 prospectuses issued in connection with IPOs completed on the TSX or TSX-V during the years 2020 to 2024. Our objective was to identify prospectuses with substantial disclosure of ESG-related issues. This threshold was met where the discussion of ESG issues went beyond, and was not limited to, discussion of (1) diversity-related issues, (2) ESG issues in relation to mandatory regulatory matters, (3) ESG issues in relation to risk factors, and (4) brief and insignificant mention of ESG issues unrelated to the issuer’s strategic objectives and/or material business operations.[1]

Detailed Analysis and Commentary

The Higher Prevalence of ESG-Related Disclosure in TSX Offerings

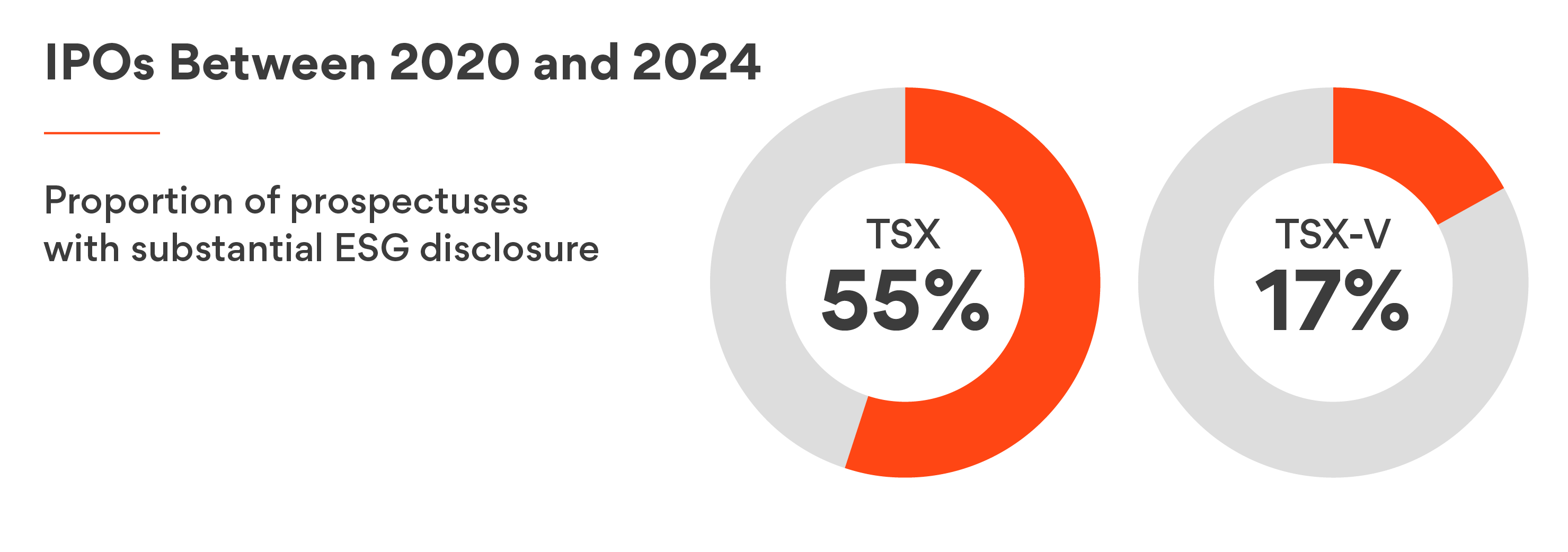

Over the last five years (2020-2024), close to 55% (26 of 47) of offerings completed on the TSX had prospectuses with substantial ESG-related disclosure. By contrast, only approximately 17% (9 of 54) of TSX-V offerings over the same period had prospectuses with substantial ESG-related disclosure.

As these disclosures of ESG-related issues have been occurring in the absence of specific ESG disclosure requirements, the clear implication is that issuers are addressing ESG issues mainly based on the general principle that a prospectus must contain full, true and plain disclosure of all material facts relating to the securities issued, and on regulatory guidance indicating that such material facts can include environmental matters.[2]

More ESG-Related Disclosure When More Funds Are Raised

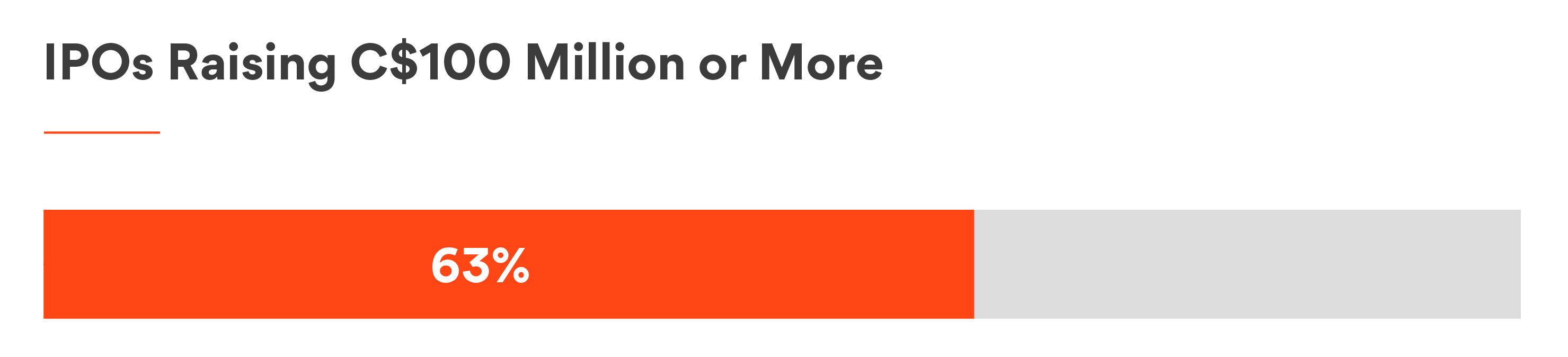

Consistent with the greater prevalence of substantial ESG-related disclosure among offerings on the TSX compared with offerings on the TSX-V, the larger the amount of funds raised, the more sophisticated and more detailed the issuer’s ESG disclosure generally is.

For example, around 63% of the prospectuses with substantial ESG-related disclosure raised C$100 million or more, while the remaining 37% of prospectuses with substantial ESG-related disclosure raised less than C$100 million.[3]

Technically, the amount of funds being raised is irrelevant to the materiality of ESG issues to the issuer’s business. We therefore assume that the less substantial disclosure of ESG issues in smaller offerings is in part driven by a cost-benefit analysis.

The Different Prevalence of ESG Topics

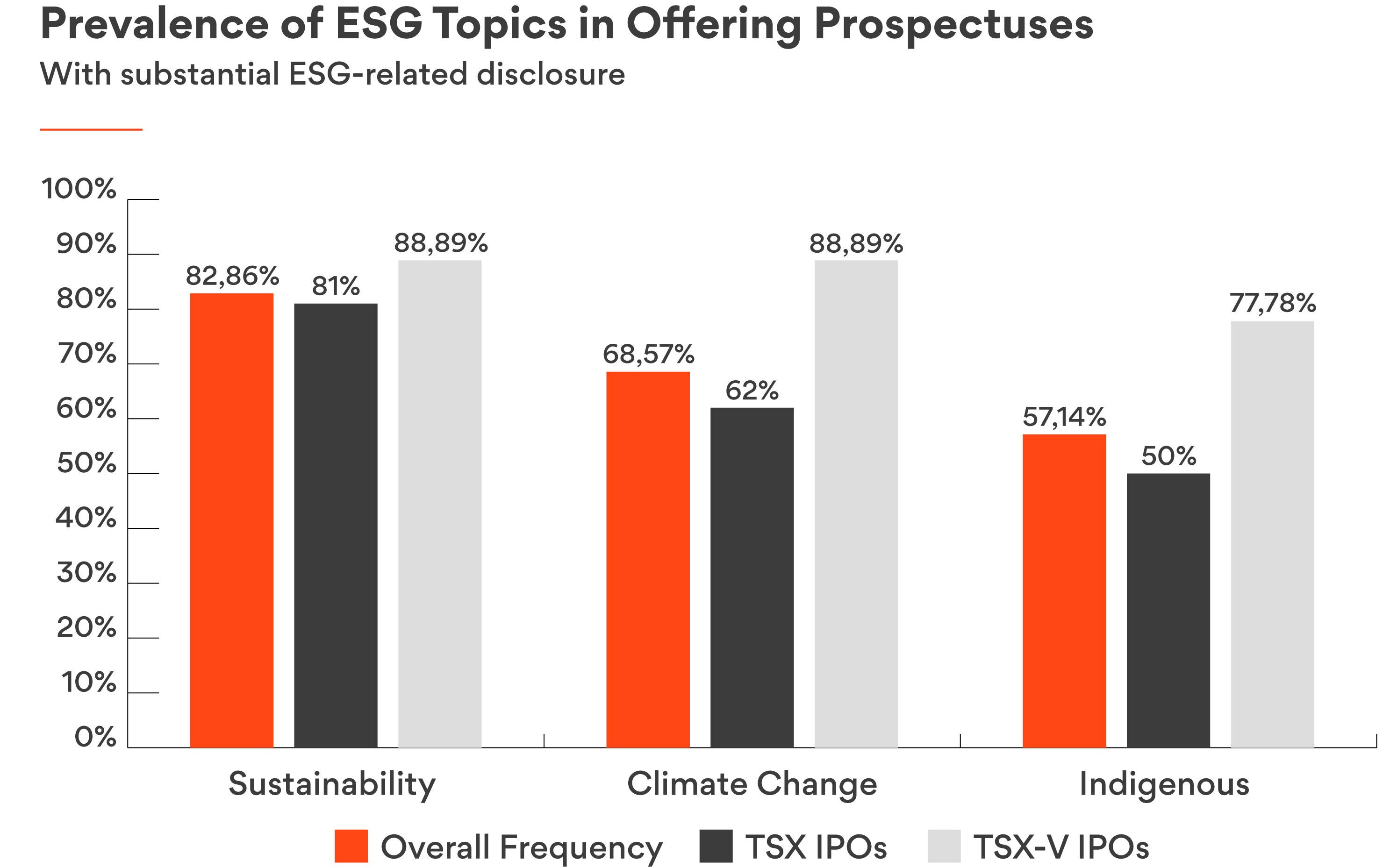

As illustrated by the following table, certain ESG issues are more likely to be addressed in offering prospectuses than others. The most common is sustainability issues generally, followed by climate change-related issues and Indigenous-related issues, respectively.

| ESG Issue | Overall Frequency in Offerings | Frequency in TSX Offerings | Frequency in TSX-V Offerings |

| Sustainability | 83% | 81% | 89% |

| Climate Change | 69% | 62% | 89% |

| Indigenous | 57% | 50% | 78% |

Interestingly, while substantial ESG-related disclosure is more common in offerings on the TSX, offerings on the TSX-V that include substantial ESG-related disclosure tend to include discussion of a wider array of ESG issues than their counterparts on the TSX. The explanation here appears to be that, in our sample, the offerings on the TSX-V with substantial ESG disclosure were primarily in the mining and oil & gas sectors, where company operations are by their nature more likely to raise ESG-related considerations than operations in other, less environmentally-intensive industries.

The Industry-Agnostic Nature of ESG-Related Disclosure

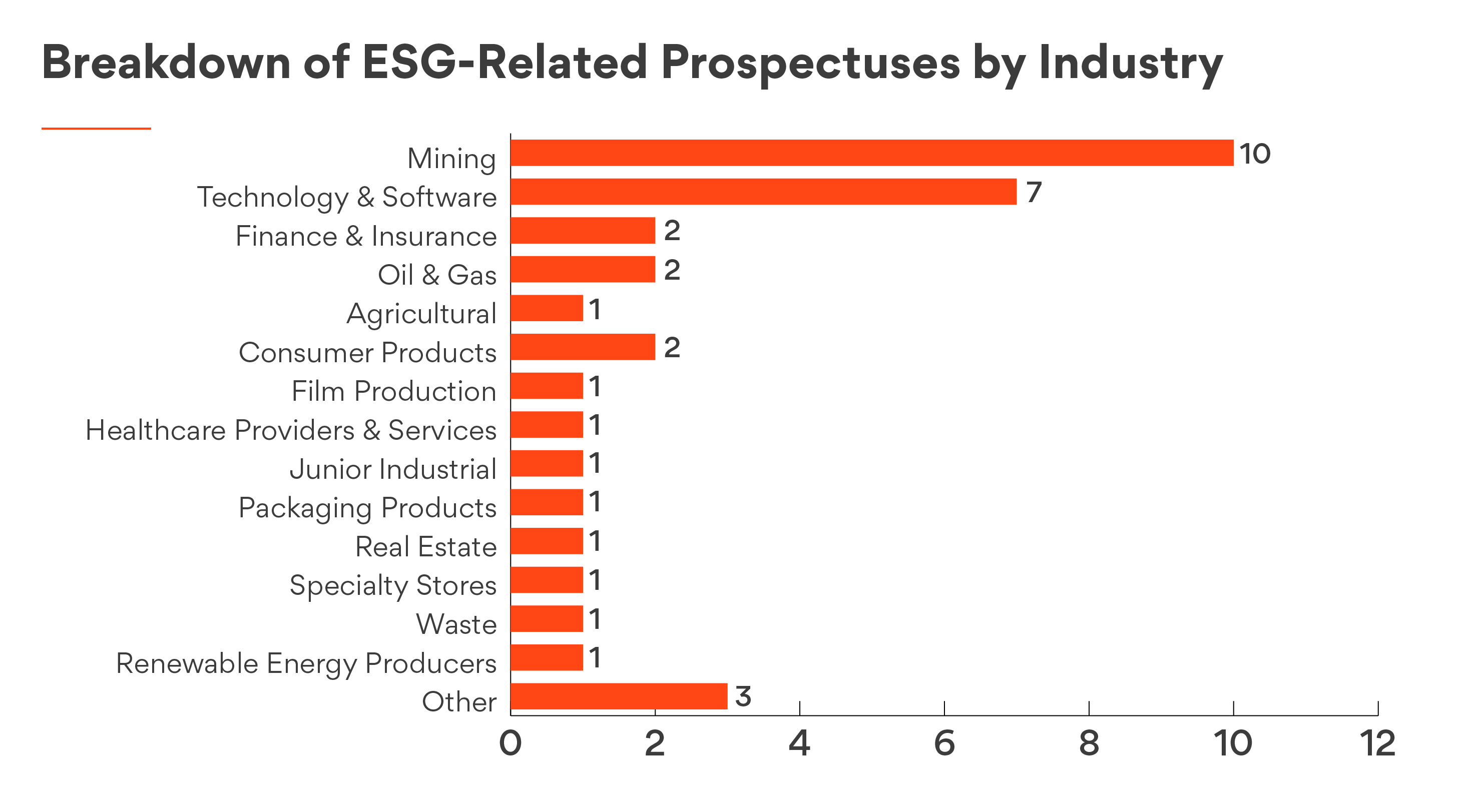

Substantial ESG-related disclosure in IPO prospectuses occurred in a variety of industries: the 35 prospectuses that included substantial ESG-related disclosure were spread across 15 of 20 different industry categories.[4] This indicates that ESG-related disclosure in prospectuses has generally been industry-agnostic and is more a function of (1) the issuer’s particular circumstances, and/or (2) per our previous statistics, the amount of funds being raised and the issuer’s individual cost-benefit analysis in connection with same.[5]

In terms of the frequency of substantial ESG-related disclosure, the industry that scored the highest was Technology & Software, with such disclosure occurring in 47% (7 of 15) prospectuses. The explanation here may be that, consistent with our other findings, all but one of the Technology & Software offerings (1) occurred on the TSX, and (2) raised relatively high amounts (compared to the average raise of all the offerings in our sample).

Also noteworthy is substantial ESG-related disclosure occurred in only 35% (10 of 29) of mining prospectuses. Given that mining operations are inherently physically and environmentally intensive, we would have expected this percentage to be higher. However, consistent with our other findings, all of the mining offerings that did not include substantial ESG disclosure (1) occurred on the TSX-V, and (2) raised relatively lower amounts (compared to the average raise of all the offerings in our sample). Also, and as further discussed below, more than 76% (22 of 29) of mining prospectuses addressed ESG issues in the applicable “Risk Factors” section.

2021: The Pinnacle of ESG-Related Disclosure?

The regularity of substantial ESG-related disclosure in prospectuses varied considerably across the different years in our study. For example, the practice was particularly common in 2021, which was also the year of the largest number of offerings.

| Year | Number of Offerings | Approximate Percentage of Offerings with Substantial ESG-related Disclosure |

| 2020 | 17 | 24% |

| 2021 | 59 | 42% |

| 2022 | 15 | 27% |

| 2023 | 6 | 0% |

| 2024 | 4 | 50%[6] |

This cannot be attributed to 2021 having the largest capital raises, since the approximate average raise of offerings in 2020 was significantly higher compared to the approximate average capital raise of offerings in 2021. Contributing factors may therefore have been at least twofold. First, that ESG-related issues were a particularly prominent concern among investors and the market generally around that time.[7] Second, as often occurs in market practice, there may have been a “snowball” effect whereby the more regular and/or more detailed disclosure of ESG issues in earlier prospectuses encouraged similar and more widespread practices in later prospectuses.

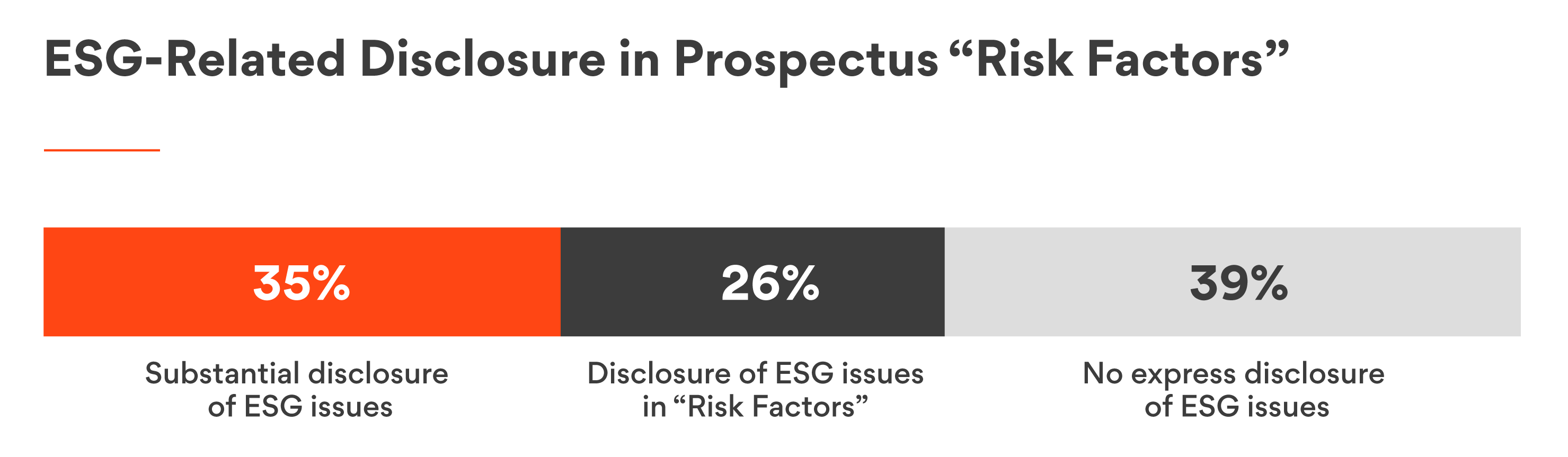

ESG-Related Disclosure in Prospectus “Risk Factors”

Of the prospectuses that did not include substantial ESG-related disclosure (66 of 101), around 40% (26 of 66) of such prospectuses included general or high-level disclosure of ESG issues in the “Risk Factors” section.

The substance of the ESG-related disclosure in these “Risk Factors” tended to be relatively uniform and employ substantially similar language. This indicates a “snowball” effect (i.e., whereby disclosure of ESG issues in earlier prospectuses encouraged similar disclosure in later prospectuses) was at least in part at work. However, this also indicates that the applicable “Risk Factors” were considered by the issuers to be material under existing general disclosure requirements.

Concluding Comments

The release of NI 51-107, if it occurs, will be a significant change for reporting issuers in Canada. The balanced approach that the CSA indicated it intends to take will determine how the market will react to the new rules, especially in the current context where geopolitical challenges are creating uncertainty around ESG regulations, first and foremost in the U.S., but also in Europe and other regions. In its latest market update, the CSA mentioned that it will continue to monitor international developments related to climate-related disclosure. Given that the United States is threatening to impose tariffs on Canadian exports, which could negatively impact the Canadian economy, the CSA may be less inclined to impose additional burdens on issuers.